As filed with the U.S. Securities and Exchange Commission on April 2, 2026.

Registration Statement No. 333-290714

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

__________________________________________

NO. 1

TO

FORM F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

__________________________________________

__________________________________________

| | 1040 | Not Applicable | ||

| (State or other jurisdiction of | (Primary standard industrial | (I.R.S. Employer |

Namib Minerals

Suite 210, 2nd Floor, Windward III, Regatta Office Park, PO Box 500,

Grand Cayman, Cayman Islands, KY1-1106

Tel: (345) 769-4909

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

__________________________________________

Cogency Global Inc.

122 East 42nd Street, 18th Floor

New York, NY 10168

Tel: (212) 947-7200

(Name, address, including zip code, and telephone number, including area code, of agent for service)

__________________________________________

Copies to:

|

Barbara A. Jones, Esq. Greenberg Traurig, LLP Suite 1900 1840 Century Park Blvd. Los Angeles, CA 90067 Tel: (310) 586-7700 |

__________________________________________

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933.

Emerging growth company

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 7(a)(2)(B) of the Securities Act.

____________

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

This Post-Effective Amendment No. 1 to Form F-1 shall hereafter become effective in accordance with Section 8(c) of the Securities Act of 1933, as amended (the Securities Act”), on such date as the Securities and Exchange Commission, acting pursuant to Section 8(c) of the Securities Act, may determine.

EXPLANATORY NOTE

This Post-effective Amendment No. 1 to the Registration Statement on Form F-1 (File No. 333-290714) (as amended, the “Registration Statement”) of Namib Minerals (the “Registrant”), which became effective pursuant to Section 8(a) of the Securities Act on October 23, 2025, is being filed pursuant to the undertakings in Item 9 of Form F-1 and includes the Registrant’s audited consolidated financial statements as of December 31, 2025 and 2024 and for each year in the three-year period ended December 31, 2025, and certain other updates.

No additional securities are being registered under this Post-effective Amendment No. 1. The applicable registration fees were paid at the time of the original filing of the Registration Statement.

The information in this preliminary prospectus is not complete and may be changed. A registration statement relating to these securities has been filed with the Securities and Exchange Commission. The Selling Shareholder may not sell these securities until such registration statement is effective. This preliminary prospectus is not an offer to sell or the solicitation of an offer to buy these securities, and there shall not be any sale of these securities in any jurisdiction in which such offer, solicitation, or sale would be unlawful.

SUBJECT TO COMPLETION, DATED APRIL 2, 2026

PRELIMINARY PROSPECTUS

![]()

Namib Minerals

Up to 1,750,000 Ordinary Shares by the Selling Shareholder

This prospectus relates to the offer and sale from time to time by Cohen & Company Securities, LLC (the “Selling Shareholder”) of up to 1,750,000 ordinary shares, par value $0.0001 per share (the “Ordinary Shares”), of Namib Minerals (the “Company”) that may be issued pursuant to the Amended and Restated Promissory Note with a face value of $3.5 million (the “Promissory Note”), dated as of December 9, 2025, issued by the Company to the Selling Shareholder. The Company issued the Promissory Note to the Selling Shareholder in connection with amounts due and payable for previously provided investment banking services. The Ordinary Shares that may be sold by the Selling Shareholder are collectively referred to in this prospectus as the “Resale Shares.” The Selling Shareholder is a registered broker dealer and may be deemed to be an “underwriter” within the meaning of the Securities Act of 1933, as amended (the “Securities Act”). The Selling Shareholder has informed the Company that it does not have any written or oral agreement or understanding, directly or indirectly, with any person to distribute any Ordinary Shares.

Pursuant to the terms of the Promissory Note, the Company will pay the Selling Shareholder, at its discretion, in either cash or Ordinary Shares with the issue price of the Ordinary Shares (the “Issue Price”) being calculated as the lesser of (i) 95% of the closing price on the Nasdaq Stock Market LLC (“Nasdaq”) of the Ordinary Shares on the Trading Day (as defined herein) immediately preceding the applicable payment date and (ii) the arithmetic average of the Daily VWAP (as defined herein) for the five (5) Trading Days ending on the Trading Day immediately preceding the applicable payment date. A significant portion of the Ordinary Shares being registered for resale may be acquired by the Selling Shareholder at prices below the current market price of our Ordinary Shares. As a result, investors may experience substantial dilution and a decline in the value of the Ordinary Shares they purchase from the Selling Shareholder in this offering as a result of future issuances made by us to the Selling Shareholder in the event the Issue Price at issuance is lower than the price such investors paid for their shares. The actual number of Ordinary Shares issuable by us under the Promissory Note will vary depending on the then-current market price of our Ordinary Shares at the times of issuance. As of April 1, 2026, the Company has issued 805,228 Ordinary Shares to the Selling Shareholder under the Promissory Note.

We are registering the resale of the Ordinary Shares covered by this prospectus pursuant to the registration rights that we have granted to the Selling Shareholder in connection with the Promissory Note. We will not receive any proceeds from the sale of the Resale Shares by the Selling Shareholder.

We do not know when or in what amount the Selling Shareholder may sell the Resale Shares hereunder following the effective date of the registration statement of which this prospectus forms a part. The Resale Shares being offered for resale pursuant to this prospectus by the Selling Shareholder represent approximately 3.2% of Ordinary Shares outstanding (assuming all such shares are issued). For information on securities eligible for future sale, including securities not covered by this resale prospectus, see the sections entitled “Risk Factors” and “Securities Eligible for Future Sale” in this prospectus.

We will bear all costs, expenses and fees in connection with the registration of the resale of the Resale Shares. The Selling Shareholder will bear all commissions and discounts, if any, attributable to its sales of the Resale Shares. This prospectus also covers any additional securities that may become issuable by reason of share splits, share dividends or similar transactions.

Our registration of the securities covered by this prospectus does not mean that the Selling Shareholder will offer or sell any Ordinary Shares. The Selling Shareholder may offer and sell the securities covered by this prospectus in a number of different ways and at varying prices. We provide more information about how the Selling Shareholder may sell the shares in the section entitled “Plan of Distribution.”

You should read this prospectus and any prospectus supplement or amendment carefully before you invest in the Ordinary Shares.

Our Ordinary Shares are listed on the Nasdaq Global Market under the symbol “NAMM,” and our Warrants are listed on the Nasdaq Capital Market under the symbol “NAMMW.” On March 31, 2026, the closing trading prices of our Ordinary Shares and Warrants were $2.31 and $0.135, respectively.

Investing in our Ordinary Shares or Warrants involves a high degree of risk. Before buying any Ordinary Shares or Warrants you should carefully read the discussion of material risks of investing in such securities in “Risk Factors” beginning on page 7 of this prospectus.

NEITHER THE U.S. SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THESE SECURITIES OR DETERMINED IF THIS PROSPECTUS IS TRUTHFUL OR COMPLETE. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

This prospectus is dated , 2026.

TABLE OF CONTENTS

|

Page |

||

|

ii |

||

|

iii |

||

|

iv |

||

|

v |

||

|

x |

||

|

xiii |

||

|

1 |

||

|

6 |

||

|

7 |

||

|

39 |

||

|

40 |

||

|

41 |

||

|

42 |

||

|

78 |

||

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

85 |

|

|

103 |

||

|

107 |

||

|

113 |

||

|

114 |

||

|

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT |

129 |

|

|

131 |

||

|

132 |

||

|

139 |

||

|

140 |

||

|

140 |

||

|

140 |

||

|

141 |

||

|

F-1 |

i

ABOUT THIS PROSPECTUS

This document, which forms part of a registration statement on Form F-1 filed with the SEC by the Company, constitutes a prospectus of the Company under Section 5 of the Securities Act of 1933, as amended (the “Securities Act”).

Neither we nor the Selling Shareholder have authorized anyone to provide any information or to make any representations other than the information contained in this prospectus, any amendment or supplement to this prospectus or in any free writing prospectus prepared by or on behalf of us or to which we may have referred you. We and the Selling Shareholder take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We and the Selling Shareholder have not authorized any other person to provide you with different or additional information. Neither we nor the Selling Shareholder are making an offer to sell the securities covered by this prospectus in any jurisdiction where the offer or sale is not permitted. This offering is being made in the United States and elsewhere solely on the basis of the information contained in this prospectus. You should assume that the information appearing in this prospectus is accurate only as of the date on the front cover of this prospectus, regardless of the time of delivery of this prospectus or any sale of the securities covered by this prospectus. Our business, financial condition, results of operations and prospects may have changed since the date on the front cover of this prospectus. This prospectus is not an offer to sell or the solicitation of an offer to buy our securities in any circumstances under which such offer or solicitation is unlawful.

We are an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012 and are therefore eligible to take advantage of certain reduced reporting requirements otherwise applicable to other public companies.

For investors outside the United States: Neither we nor the Selling Shareholder have done anything that would permit this offering or the possession or distribution of this prospectus in any jurisdiction where action for those purposes is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, this offering of securities covered by this prospectus and the distribution of this prospectus outside the United States.

Our Company is incorporated in the Cayman Islands, and we are a “foreign private issuer” under the rules of the SEC. As a foreign private issuer, we are not required to file periodic reports and financial statements with the SEC as frequently or as promptly as domestic registrants whose securities are registered under the Exchange Act. Moreover, three of our directors and executive officers are not residents of the United States, and all or a substantial portion of the assets of such persons are located outside the United States. As a result, it may not be possible for investors to effect service of process within the United States upon us or upon such persons or to enforce against them judgments obtained in U.S. courts, including judgments in actions predicated upon the civil liability provisions of the federal or state securities laws of the United States. We have been advised by our legal counsel in the Cayman Islands that it is uncertain as to whether the courts in the Cayman Islands would entertain original actions based on U.S. federal or state securities laws or enforce judgments from U.S. courts against us or our officers and directors which originated from actions alleging civil liability under U.S. federal or state securities laws. See “Enforceability of Civil Liabilities” for additional information.

ii

MARKET AND INDUSTRY DATA

Unless otherwise indicated, information contained in this prospectus or incorporated into this prospectus by reference regarding the Company’s industry and the regions in which it operates, including market research, estimates, and forecasts, is based on information obtained from industry publications and reports and forecasts provided to the Company by third-party sources. In some cases, the Company does not expressly refer to the sources from which this information is derived. This information is subject to significant uncertainties and limitations and is based on assumptions and estimates that may prove to be inaccurate. Neither we nor the Selling Shareholder can guarantee the accuracy or completeness of any such information contained in this prospectus or incorporated into this prospectus by reference. You are therefore cautioned not to give undue weight to this information.

The Company has not independently verified the accuracy or completeness of any such information. Similarly, internal surveys, industry forecasts and market research, which the Company believes to be reliable based upon its management’s knowledge of the industry, have not been independently verified. While the Company believes that the market data, industry forecasts and similar information included in this prospectus are generally reliable, such information is inherently imprecise. In addition, assumptions and estimates of the Company’s future performance and growth objectives and the future performance of its industry and the markets in which it operates are necessarily subject to a high degree of uncertainty and risk due to a variety of factors, including those discussed under the headings “Risk Factors,” “Cautionary Note Regarding Forward-Looking Statements,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this prospectus.

iii

FINANCIAL STATEMENT PRESENTATION

References to “U.S. dollars” and “US$” in this prospectus are to United States dollars, the legal currency of the United States. Discrepancies in any table between totals and sums of the amounts listed are due to rounding. Certain amounts and percentages have been rounded; consequently, certain figures may add up to be more or less than the total amount and certain percentages may add up to be more or less than 100% due to rounding. In particular and without limitation, amounts expressed in millions contained in this prospectus have been rounded to a single or two decimal places for the convenience of readers.

The historical financial statements of Namib Minerals are prepared in accordance with IFRS Accounting Standards, as issued by International Accounting Standards Board (“IFRS”). Namib Minerals’ fiscal year ends on December 31 of each year, as does its reporting year. Namib Minerals was incorporated on May 27, 2024, and its initial fiscal year ended on December 31, 2024. Namib Minerals’ most recent fiscal year ended on December 31, 2025. See Note 2 to Namib Minerals’ audited financial statements as of December 31, 2025, and 2024 and for each year in the three-year period ended December 31, 2025, included elsewhere in this prospectus, for a discussion of the basis of presentation of Namib Minerals’ financial statements.

iv

TECHNICAL MINING INFORMATION AND SPECIAL TERMS

Cautionary Note Regarding Presentation of Mineral Reserve and Mineral Resource Estimates

On October 31, 2018, the SEC adopted Subpart 1300 (17 CFR 229.1300) of Regulation S-K (“Regulation S-K 1300”), along with the amendments to related rules and guidance, in order to modernize the property disclosure requirements for mining registrants under the Securities Act and the Exchange Act. Registrants engaged in mining operations must comply with Regulation S-K 1300 for fiscal years beginning on or after January 1, 2022. Mineral resource and mineral reserve estimates were prepared by the Company based on available data at the time of calculation and are inherently uncertain, involve subjective judgment about many relevant factors and may be materially affected by, among other things, environmental, permitting, legal, title, taxation, socio-political, marketing, or other relevant risks, uncertainties, contingencies and factors. Until mineral deposits are actually mined and processed, mineral resources and mineral reserves must be considered as estimates only.

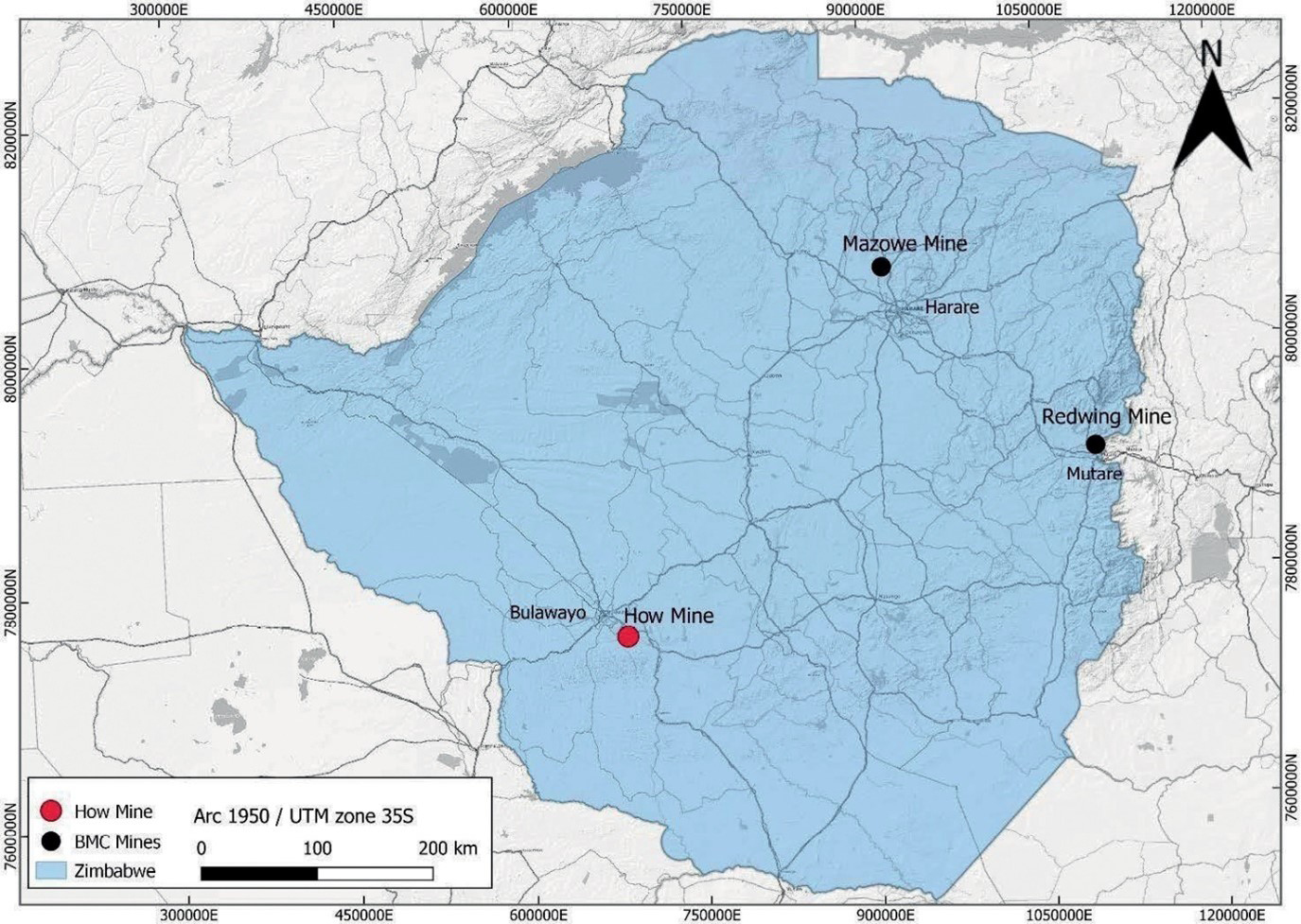

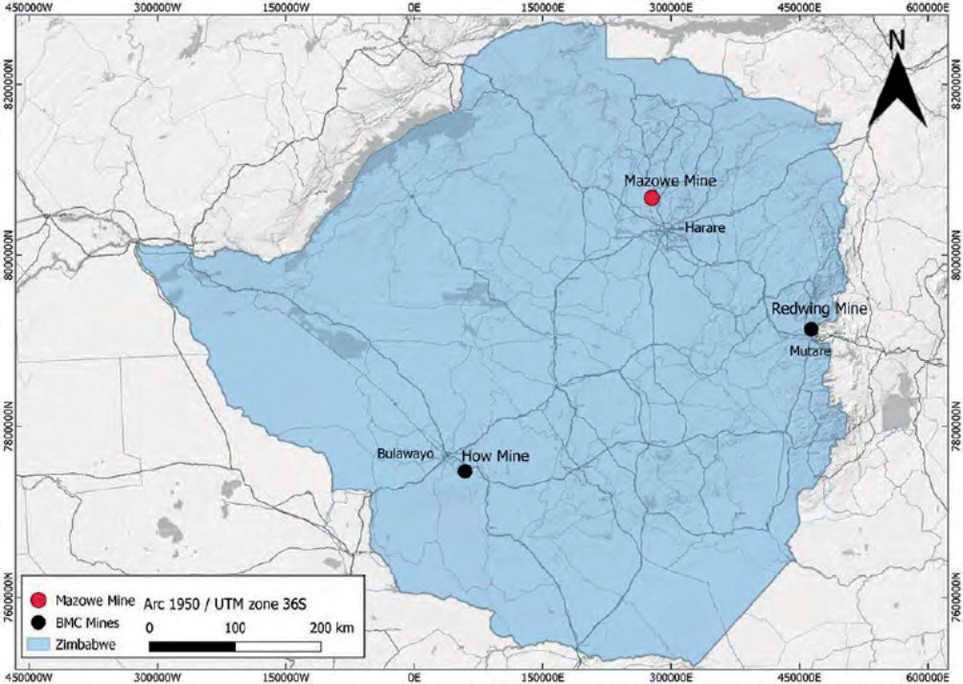

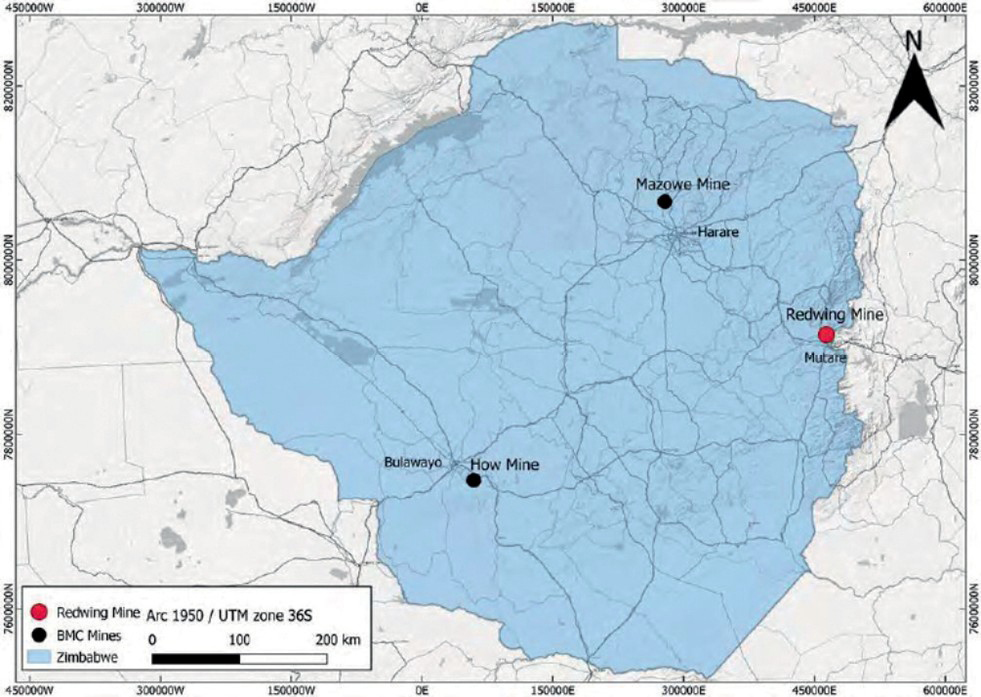

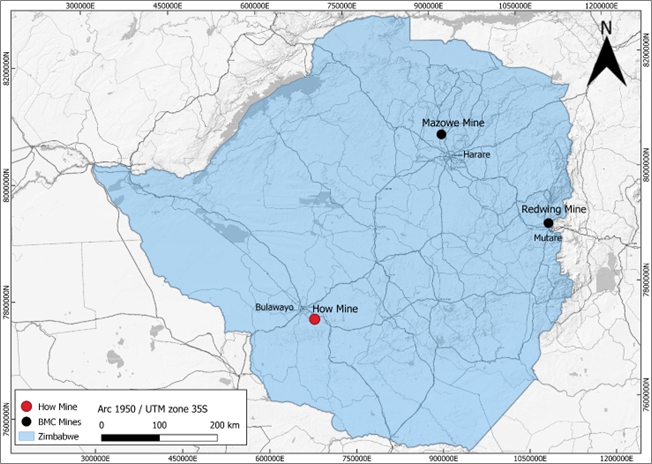

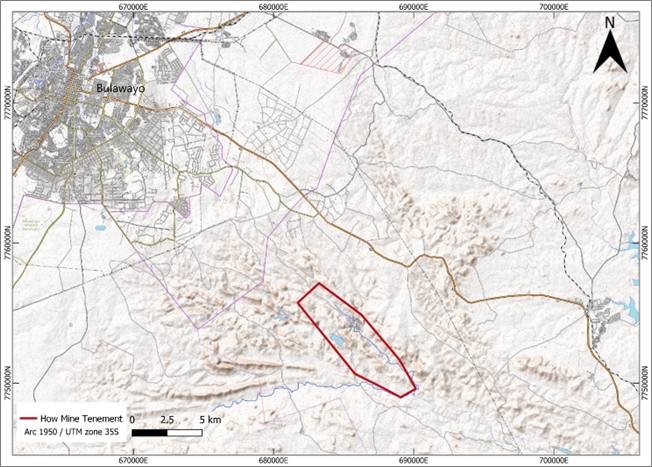

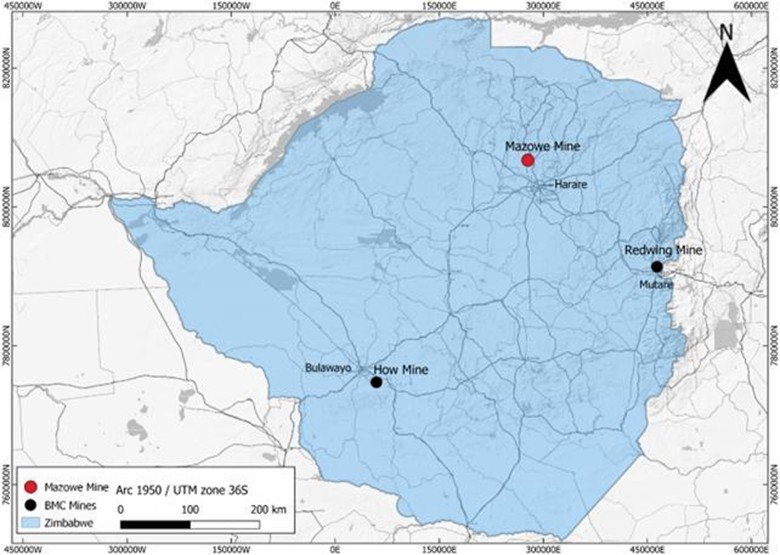

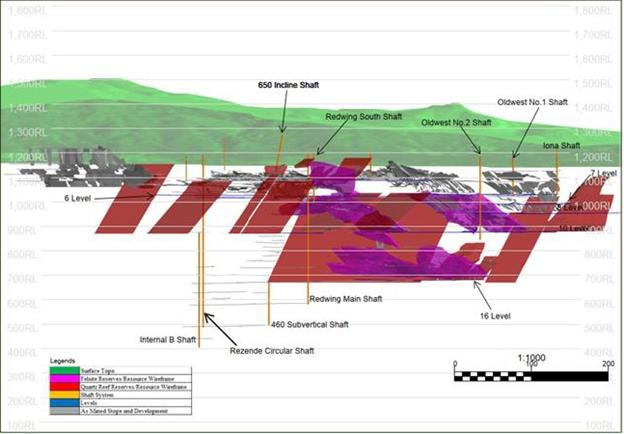

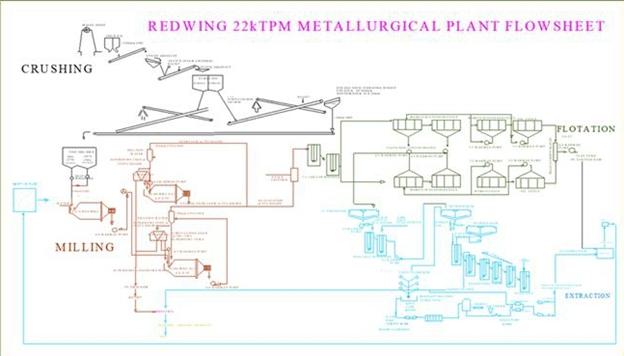

The Company owns three mines, of which only the How Mine is currently in commercial operation. There is no commercial production at the Mazowe Mine or the Redwing Mine, as each mine has been on care and maintenance since August 2018 and April 2019, respectively.

The Company has inferred, indicated, and measured mineral resources, and certain of the indicated and measured mineral resources are classified as probable and proven mineral reserves. An inferred mineral resource has a lower level of confidence than that of an indicated or measured mineral resource and may not be converted to a mineral reserve. You are cautioned that, except for that portion of mineral resources classified as mineral reserves, mineral resources do not have demonstrated economic viability. Specifically, inferred mineral resources have a high degree of uncertainty as to their existence and as to whether they can be economically or legally mined. Under Regulation S-K 1300, estimates of inferred mineral resources may not form the basis of an economic analysis. It cannot be assumed that all or any part of an inferred mineral resource will ever be upgraded to a higher category. Such upgrade would require a significant amount of exploration. Therefore, you are cautioned not to assume that all or any part of an inferred mineral resource can be economically or legally mined, or that it will ever be upgraded to a higher category. Likewise, you are cautioned not to assume that all or any part of measured or indicated mineral resources not already classified as mineral reserves will ever be upgraded to mineral reserves.

Special Mining Terms

“Assay” means chemical test performed on a sample of ores or minerals to determine the amount of valuable metals contained.

“BIF” means Banded Iron Formation.

“Carbon-in-plant” or “CIP” means gold is leached conventionally from a slurry of gold ore with cyanide in agitated tanks. The leached slurry passes into the CIP circuit where carbon granules are mixed with the slurry and gold is absorbed onto the carbon. The carbon granules are separated from the slurry and treated to remove gold.

“Care and maintenance” means the processes and conditions on a closed mine site where there is potential to recommence operations at a later date.

“Concentrate” means a clean product which has been upgraded sufficiently for downstream processing or sale.

“Contained gold” means the total gold or copper content (tons multiplied by grade) of the material being described.

“Cut-off grade” or “COG” means the grade (i.e., the concentration of metal or mineral in rock) that determines the destination of the material during mining. For purposes of establishing “prospects of economic extraction,” the cut-off grade is the grade that distinguishes material deemed to have no economic value (it will not be mined in underground mining or if mined in surface mining, its destination will be the waste dump) from material deemed to have economic value (its ultimate destination during mining will be a processing facility). Other terms used in similar fashion as cut-off grade include net smelter return, pay limit, and break-even stripping ratio.

“Cyanidation” means a method of extracting exposed gold grains from crushed or ground ore by dissolving it in a weak cyanide solution. May be carried out in tanks inside a mill or in heaps of ore out of doors.

v

“Decline” means an inclined underground access way.

“Deposit” means an informal term for an accumulation of mineralization or other valuable earth material of any origin.

“Development” means the process of accessing an orebody through shafts or tunneling in underground mining.

“Dilution” means unmineralized rock that is, by necessity, removed along with ore during the mining process that effectively lowers the overall grade of the ore.

“Diorite” means an igneous rock formed by the solidification of molten material (magma).

“Dyke” means a long and relatively thin body of igneous rock that, while in the molten state, intruded a fissure in older rocks.

“Economically viable” means, when used in the context of Mineral Reserve determination, that the Qualified Person has determined, using a discounted cash flow analysis, or has otherwise analytically determined, that extraction of the Mineral Reserve is economically viable under reasonable investment and market assumptions.

“Elution” means the removal of the gold from the activated carbon before the zinc precipitation stage.

“Exploration” means activities associated with ascertaining the existence, location, extent, or quality of mineralized material, including economic and technical evaluation of mineralized material.

“Feasibility Study” means a comprehensive technical and economic study of the selected development option for a mineral project that includes appropriately detailed assessments of applicable modifying factors together with any other relevant operational factors and detailed financial analysis that are necessary to demonstrate at the time of reporting that extraction is reasonably justified (economically mineable). The results of the study may reasonably serve as the basis for a final decision by a proponent or financial institution to proceed with, or finance, the development of the project. The confidence level of the study will be higher than that of a prefeasibility study.

“Flotation” means a concentration of gold and gold-hosting minerals into a small mass by various techniques (e.g. collectors, frothers, agitation, air-flow) that collectively enhance the buoyancy of the target minerals, relative to unwanted gangue, for recovery into an over-flowing froth phase.

“Footwall” means the underlying side of a fault, orebody or stope.

“Geological” means relating to the study of rocks which compose the earth.

“Grade” means the quantity of ore contained within a unit weight of mineralized material generally expressed in grams per metric tonne (g/t) or ounce per short ton for gold bearing material.

“Greenschist” means a schistose metamorphic rock whose green color is due to the presence of chlorite, epidote or actinolite.

“Indicated Mineral Resource” means that part of a Mineral Resource for which quantity, grade or quality, densities, shape and physical characteristics are estimated with sufficient confidence to allow the application of modifying factors in sufficient detail to support mine planning and evaluation of the economic viability of the deposit. Geological evidence is derived from adequately detailed and reliable exploration, sampling and testing and is sufficient to assume geological and grade or quality continuity between points of observation.

“Inferred Mineral Resource” means that part of a Mineral Resource for which quantity and grade or quality are estimated based on limited geological evidence and sampling. Geological evidence is sufficient to imply, but not verify, geological and grade or quality continuity. An Inferred Mineral Resource has a lower level of confidence than that applying to an Indicated Mineral Resource and must not be converted to a Mineral Reserve. It is reasonably expected that the majority of an Inferred Mineral Resource could be upgraded to an Indicated Mineral Resource with continued exploration.

“Initial assessment (also known as concept study, scoping study, conceptual study and preliminary economic assessment)” means a preliminary technical and economic study of the economic potential of all or parts of mineralization to support the disclosure of Mineral Resource. The initial assessment must be prepared by a Qualified

vi

Person and must include appropriate assessments of reasonably assumed technical and economic factors, together with any other relevant operational factors, that are necessary to demonstrate at the time of reporting that there are reasonable prospects for economic extraction. An initial assessment is required for disclosure of Mineral Resource but cannot be used as the basis for disclosure of Mineral Reserve.

“Level” means the workings or tunnels of an underground mine that are on the same horizontal plane.

“Life-of-mine” or “LOM” means number of years for which an operation is planning to mine and treat ore and is taken from the current mine plan.

“Measured Mineral Resource” means that part of a Mineral Resource for which quantity, grade or quality, densities, shape, and physical characteristics are estimated with confidence sufficient to allow the application of modifying factors to support detailed mine planning and final evaluation of the economic viability of the deposit. Geological evidence is derived from detailed and reliable exploration, sampling and testing and is sufficient to confirm geological and grade or quality continuity between points of observation. A Measured Mineral Resource has a higher level of confidence than that applying to either an Indicated or an Inferred Mineral Resource. It may be converted to either a Proven Mineral Reserve or a Probable Mineral Reserve.

“Measures” means conversion factors from metric units to U.S. units are provided below.

|

Metric Unit |

U.S. Equivalent |

|||

|

1 tonne |

= 1 t |

= 1.10231 short tons |

||

|

1 meter |

= 1 m |

= 3.28084 feet |

||

|

1 hectare |

= 1 ha |

= 2.47105 acres |

“Metallurgy” means the science and art of separating metals and metallic minerals from their ores by mechanical and chemical processes.

“Milling/mill” means the communition of the ore, although the term has come to cover the broad range of machinery inside the treatment plant where the gold is separated from the ore.

“Mineral” means a naturally occurring homogeneous substance having definite physical properties and chemical composition and, if formed under favorable conditions, a definite crystal form.

“Mineral Reserve” means the economically mineable part of a Measured and/or Indicated Mineral Resource. It includes diluting materials and allowances for losses, which may occur when the material is mined or extracted and is defined by studies at prefeasibility or feasibility level as appropriate that include application of modifying factors. Such studies demonstrate that, at the time of reporting, extraction could reasonably be justified. The reference point at which Mineral Reserves are defined, usually the point where the ore is delivered to the processing plant, must be stated. It is important that in all situations where the reference point is different, such as for a saleable product, a clarifying statement is included to ensure that the reader is fully informed as to what is being reported.

“Mineral Resource” means a concentration or occurrence of solid material of economic interest in or on the Earth’s crust in such form, grade or quality and quantity that there are reasonable prospects for eventual economic extraction. The location, quantity, grade, continuity and other geological characteristics of a Mineral Resource are known, estimated or interpreted from specific geological evidence and knowledge, including sampling.

“Mineralization” means the presence of a target mineral in a mass of host rock.

“Modifying Factors” means considerations used to convert Mineral Resources to Mineral Reserves. These include, but are not restricted to, mining, processing, metallurgical, infrastructure, economic, marketing, legal, environmental, social, and governmental factors.

vii

“MSZ” means Mineralized Shear Zones.

“Mt” or “tonne” means metric tonne, a metric measurement of weight equivalent to 1,000 kilograms or 2,204.6 pounds.

“Ore” means a mixture of mineralized material from which at least one of the contained minerals can be mined and processed at an economic profit.

“Orebody” means a well-defined mass of mineralized material of sufficient mineral content to make extractions economically viable.

“Ounce” means one Troy ounce, which equals 31.1035 grams.

“Prefeasibility Study” means a comprehensive study of a range of options for the technical and economic viability of a mineral project that has advanced to a stage where a preferred mining method, in the case of underground mining, or the pit configuration, in the case of an open-pit, is established and an effective method of mineral processing is determined. It includes a financial analysis based on reasonable assumptions on the modifying factors and the evaluation of any other relevant factors which are sufficient for a competent person, acting reasonably, to determine if all or part of the Mineral Resource may be converted to a Mineral Reserve at the time of reporting. A prefeasibility study is at a lower confidence level than a feasibility study.

“Probable Mineral Reserve” means the economically mineable part of an Indicated, and in some circumstances, a Measured Mineral Resource. The confidence in the modifying factors applying to a Probable Mineral Reserve is lower than that applying to a Proven Mineral Reserve.

“Productivity” means an expression of labor productivity based on the ratio of ounces of gold produced per month to the total number of employees in mining operations.

“Proven Mineral Reserve” means the economically mineable part of a Measured Mineral Resource. A Proven Mineral Reserve implies a high degree of confidence in the modifying factors.

“QP” or “Qualified Person” means, in respect of the Company’s material properties, is an individual who is (1) a mineral industry professional with at least five years of relevant experience in the type of mineralization and type of deposit under consideration and in the specific type of activity that person is undertaking on behalf of the registrant; and (2) an eligible member or licensee in good standing of a recognized professional organization at the time the technical report is prepared. Regulation S-K 1300 details further recognized professional organizations and also relevant experience.

“Quartz” means a mineral compound of silicon and oxygen.

“Recovered grade” means the recovered mineral content per unit of ore treated.

“Reef” means a gold-bearing sedimentary horizon, normally a conglomerate band, which may contain economic levels of gold.

“Regulation S-K 1300” means the Subpart 1300 of Regulation S-K (17 CFR § 229.1300) which contains the SEC’s mining property disclosure requirements for mining registrants.

“Run-of mine” or “ROM” means the unprocessed mined material which consists of the rock, minerals, middlings, contamination, and impurities.

“Sampling” means taking small pieces of rock at intervals along exposed mineralization for assay (to determine the mineral content).

“SAMREC (2016)” means South African Code for the Reporting of Exploration Results, Mineral Resources and Mineral Reserves 2016 edition.

viii

“Shaft” means a structure that provides principal access to the underground workings for transporting personnel, equipment, supplies, ore and waste. A shaft is also used for ventilation and as an auxiliary exit. It is equipped with a surface hoist system that lowers and raises conveyances for men, material, and ore in the shaft. A shaft generally has more than one conveyancing compartment.

“Smelting” means a thermal processing whereby molten metal is liberated from beneficiated mineral or concentrate with impurities separating as lighter slag.

“Stockpile” means a store of unprocessed ore.

“Stope” means the underground excavation within the orebody where the main gold production takes place.

“Strike” means the direction, or bearing from true north, of a vein or rock formation measured on a horizontal surface.

“Tailings” means finely ground rock of low residual value from which valuable minerals have been extracted is discarded and stored in a designed dam facility.

“Tonnage” means quantities where the ton or tonne is an appropriate unit of measure. Typically used to measure reserves of gold-bearing material in situ or quantities of ore and waste material mined, transported or milled.

“Trend” means the arrangement of a group of ore deposits or a geological feature or zone of similar grade occurring in a linear pattern.

“Underground mining” means the extraction of rocks, minerals and industrial materials, other than coal, oil and gas, from the earth by developing entries or shafts from the surface to the seam or deposit before recovering the product by underground extraction methods.

“Waste” means material that contains insufficient mineralization for consideration for future treatment and, as such, is discarded.

“Yield” means the actual grade of ore realized after the mining and treatment process.

ix

FREQUENTLY USED TERMS

In this document:

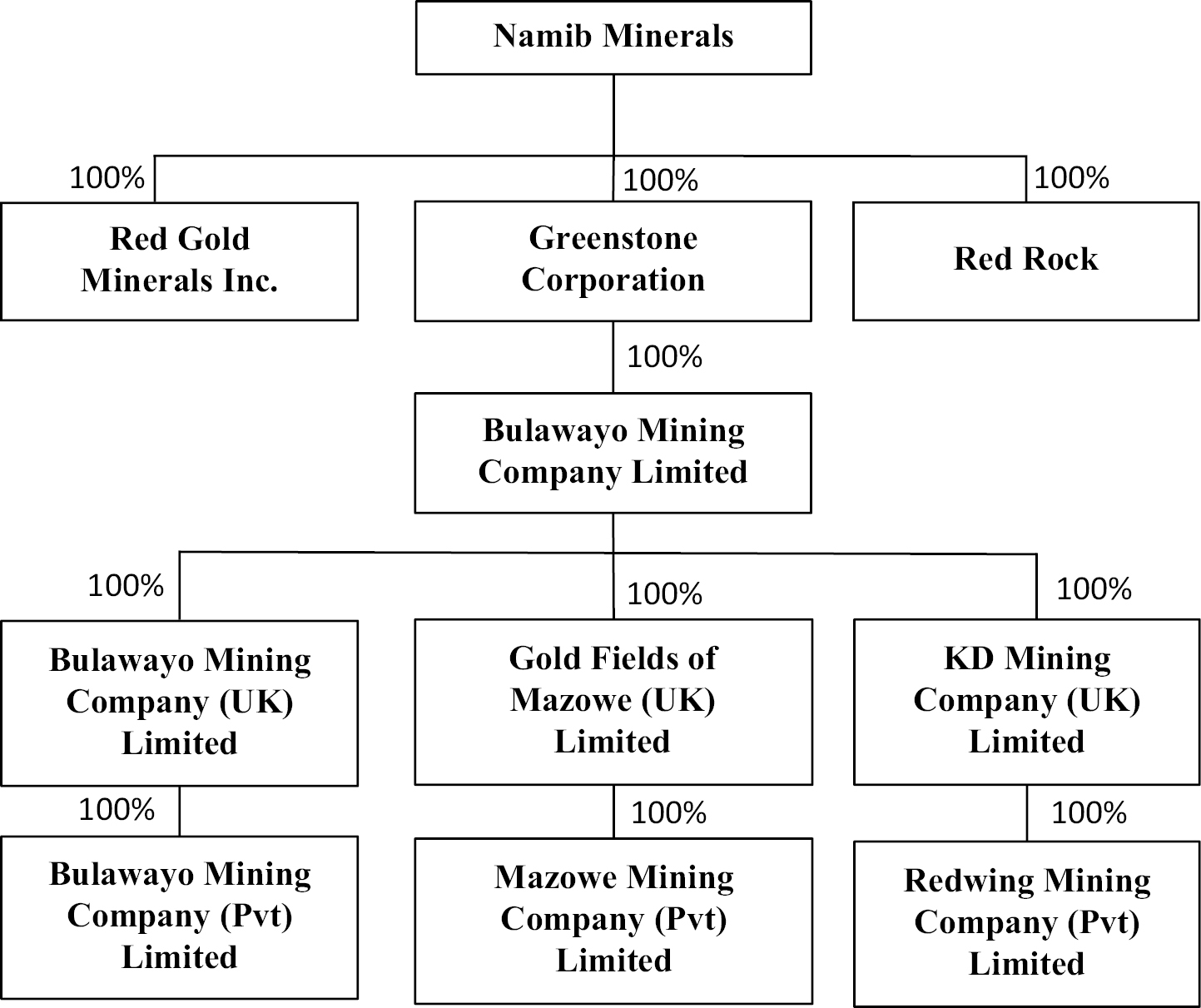

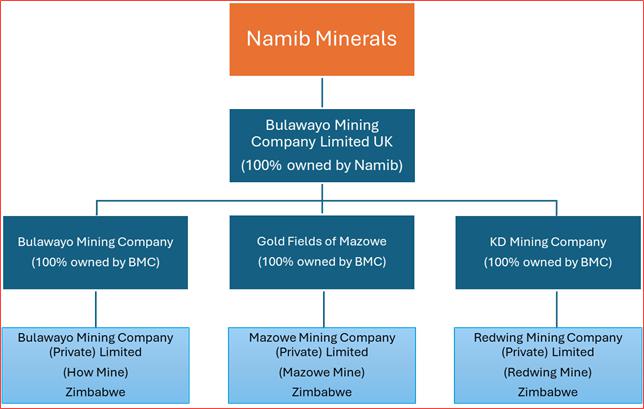

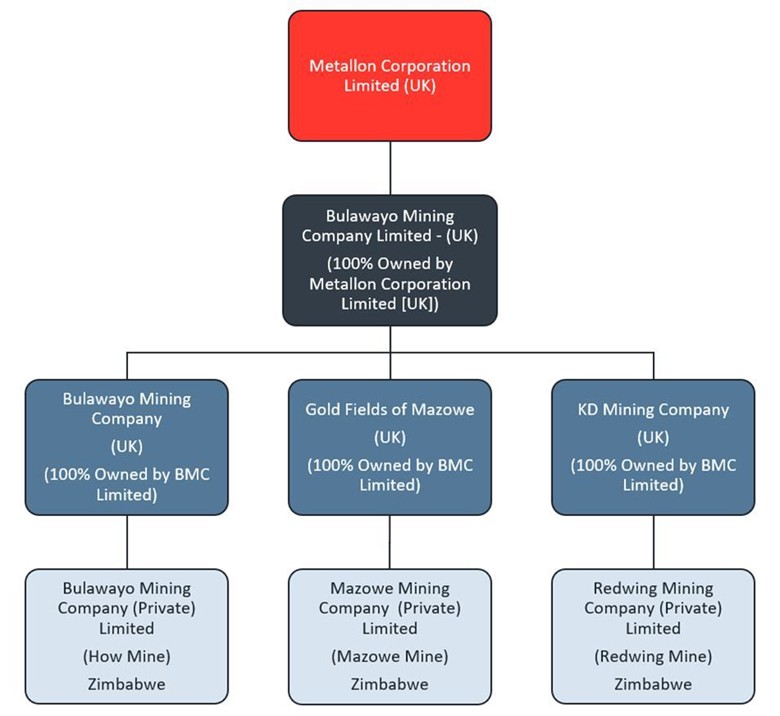

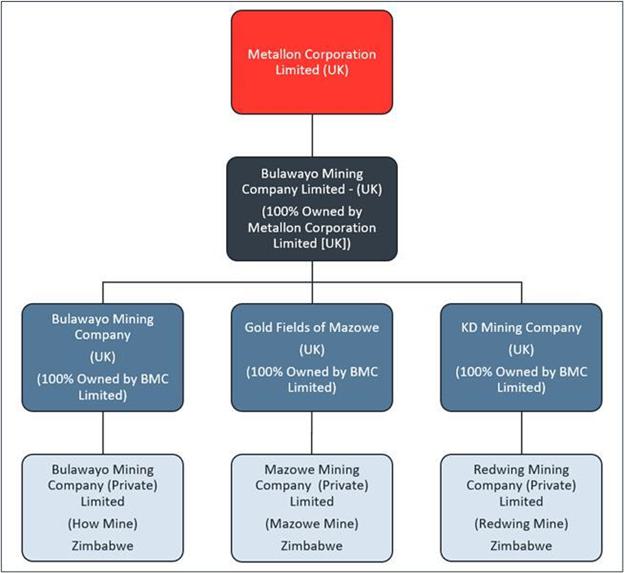

“BMC” means Bulawayo Mining Company Limited, a private company incorporated under the laws of England and Wales.

“Business Combination” means the transactions contemplated by the Business Combination Agreement.

“Business Combination Agreement” means the Business Combination Agreement, dated as of June 17, 2024, as amended, and as may be further amended, by and among Red Rock, Greenstone, the Company, SPAC Merger Sub, and Greenstone Merger Sub.

“Cayman Islands Companies Act” means the Companies Act (As Revised) of the Cayman Islands.

“Closing” means the consummation of the Business Combination.

“Closing Date” means June 5, 2025.

“Code” means the Internal Revenue Code of 1986, as amended.

“Company” or “Namib Minerals” means Namib Minerals, an exempted company limited by shares incorporated under the laws of the Cayman Islands.

“Company Board” means the board of directors of the Company.

“Company Organizational Documents” means the second amended and restated memorandum and articles of association of the Company, as amended, modified, or supplemented from time to time.

“Continental” means Continental Stock Transfer & Trust Company, a limited purpose trust company, as the Company’s transfer agent and warrant agent.

“COVID-19” means the novel coronavirus known as SARS-CoV-2 or COVID-19, and any evolutions, mutations thereof or related or associated epidemics, pandemic, or disease outbreaks.

“Daily VWAP” means, for any Trading Day, the per share volume-weighted average price of the Ordinary Shares as displayed under the heading “Bloomberg VWAP” on the Bloomberg page for the Company (or, if such page is not available, its equivalent successor page) in respect of the period from the scheduled open of trading until the scheduled close of trading of the primary trading session on such Trading Day (or, if such volume-weighted average price is unavailable, the market value of one Ordinary Shares on such Trading Day, determined, using a volume-weighted average price method, by a nationally recognized independent investment banking firm selected by the Selling Shareholder). The Daily VWAP will be determined without regard to after-hours trading or any other trading outside of the regular trading session.

“DRC” means the Democratic Republic of Congo.

“Earnout Period” means the period between the Closing Date and the eighth (8th) anniversary of the Closing Date.

“Earnout Shares” means up to 30,000,000 Ordinary Shares that may be issued by the Company to the Former Greenstone Shareholders during the Earnout Period pursuant to the terms of the Business Combination Agreement.

“Exchange Act” means the Securities Exchange Act of 1934, as amended.

“Fidelity” means Fidelity Gold Refinery (Private) Limited, a company which is controlled by the Zimbabwean authorities.

“Former Greenstone Shareholders” means the holders of Greenstone’s ordinary shares immediately prior to the Business Combination.

“Founder Shares” mean the Class B common stock of Red Rock, par value $0.0001 per share.

x

“Greenstone” means Greenstone Corporation, an exempted company limited by shares incorporated under the laws of the Cayman Islands.

“Greenstone Merger Sub” means Cayman Merger Sub Ltd., an exempted company limited by shares incorporated under the laws of the Cayman Islands and previously a direct wholly-owned subsidiary of the Company prior to the Business Combination.

“HCG” means Hennessy Capital Group LLC, a Delaware limited liability company.

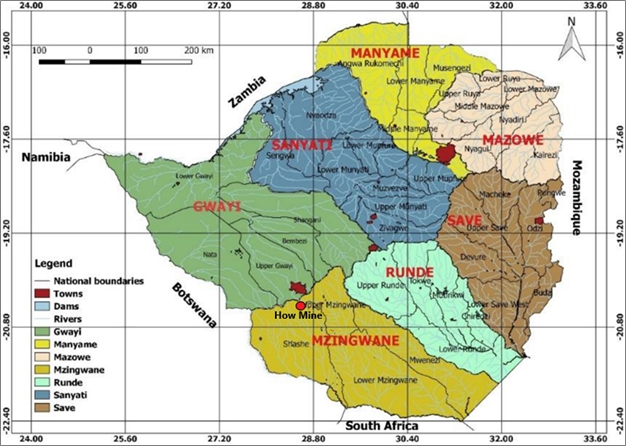

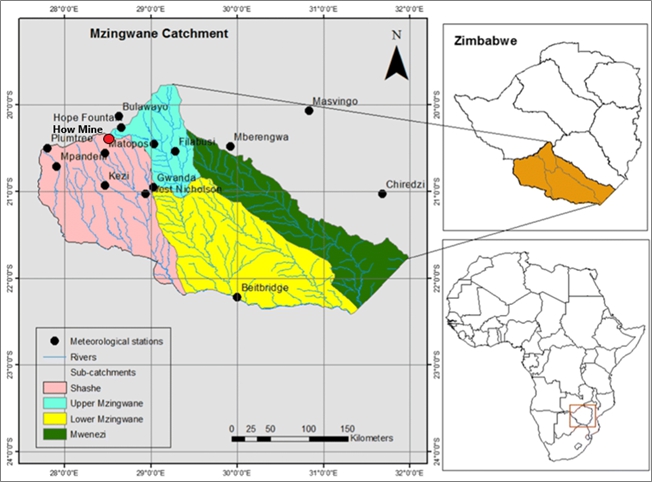

“How Mine” means the gold mine that is owned and operated by the How Mining Company in the entire mining area under the How Mine Lease, being the mining operations, the gold processing plant operations, and all operations and activities incidental thereto and related infrastructure established to access and mine minerals.

“How Mine Lease” means the mining lease by and between the Mining Affairs Board of Zimbabwe and the How Mining Company.

“How Mining Company” means Bulawayo Mining Company (Private) Limited, a Zimbabwe private limited company.

“IASB” means the International Accounting Standards Board.

“IFRS” means the International Financial Reporting Standards, as issued by the International Accounting Standards Board.

“Initial Shareholders” mean holders of Founder Shares before the Business Combination, which include (i) the SPAC Sponsor, with such limited liability company member interests being beneficially owned by Daniel J. Hennessy and Thomas D. Hennessy, the son of Daniel J. Hennessy, as the managing members of HCG, (ii) Anna Brunelle, (iii) Sidney Dillard, (iv) Walter Roloson, (v) John Zimmerman, and (vi) Rick Fearon.

“IPO” means Red Rock’s initial public offering of its units, consummated on October 1, 2021.

“Khumalo” means Mzilikazi Godfrey Khumalo.

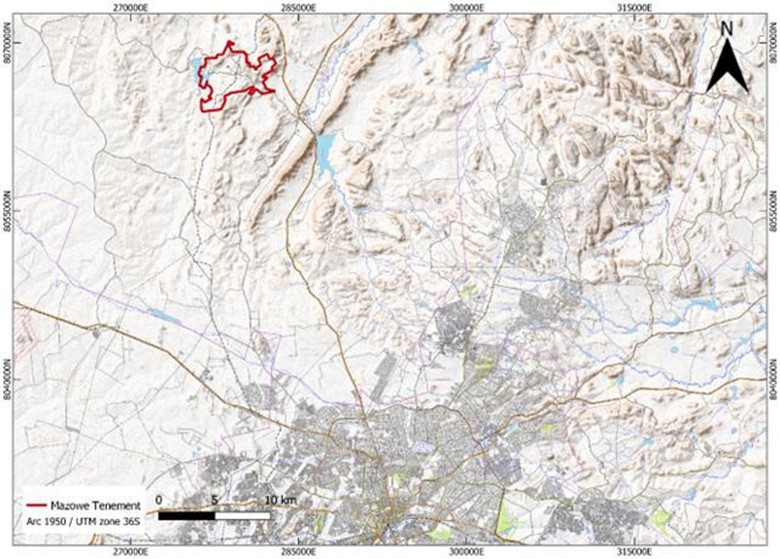

“Mazowe Mine” means the gold mine being, and to be, redeveloped, constructed, owned and operated by the Mazowe Mining Company in the entire mining area under the Mazowe Mine Lease, being the mining operations, the gold processing plant operations, and all operations and activities incidental thereto and related infrastructure established to access and mine minerals.

“Mazowe Mine Lease” means the mining lease by and between the Mining Affairs Board of Zimbabwe and the Mazowe Mining Company.

“Mazowe Mining Company” means Mazowe Mining Company (Private) Limited, a Zimbabwe private limited company (formerly known as Gold Fields of Mazowe (Private) Limited).

“Nasdaq” means The Nasdaq Stock Market LLC.

“PCAOB” means the Public Company Accounting Oversight Board and any division or subdivision thereof.

“Polar” means Polar Multi-Strategy Master Fund.

“Polar Shares” means 880,000 Ordinary Shares that were issued to Polar in a private placement pursuant to the Polar Subscription Agreements.

“Polar Subscription Agreements” means (1) a certain subscription agreement, dated October 13, 2023, by and among Red Rock, HCG, the SPAC Sponsor and Polar (“Polar Subscription Agreement I”) and (2) a certain subscription agreement, dated January 16, 2024, by and among Red Rock, the SPAC Sponsor, Daniel J. Hennessy and Polar (“Polar Subscription Agreement II”).

“Promissory Note” means that certain Amended and Restated Promissory Note, dated December 9, 2025, with a face value of $3.5 million, issued by the Company to the Selling Shareholder.

“RBZ” means the Reserve Bank of Zimbabwe.

xi

“Red Rock” or “SPAC” means Red Rock Acquisition Corporation, a Delaware corporation formerly known as Hennessy Capital Investment Corp. VI.

“Redwing Mine” means the gold mine being, and to be, redeveloped, constructed, owned, and operated by the Redwing Mining Company in the entire mining area under the Redwing Mine Lease, being the mining operations, the gold processing plant operations, and all operations and activities incidental thereto, and related infrastructure established to access and mine minerals.

“Redwing Mine Lease” means the mining lease between the Mining Affairs Board of Zimbabwe and the Redwing Mining Company.

“Redwing Mining Company” means Redwing Mining Company (Private) Limited, a Zimbabwe private limited company.

“Registration Rights and Lock-up Agreement” means that certain registration rights and lock-up agreement, dated June 5, 2025, by and among Namib Minerals, Red Rock, the Initial Shareholders and the other securityholders party thereto.

“RTG” means the Zimbabwe dollar.

“Sarbanes-Oxley Act” means the Sarbanes-Oxley Act of 2002, as amended.

“SEC” means the U.S. Securities and Exchange Commission.

“Securities Act” means the Securities Act of 1933, as amended.

“SPAC Merger Sub” means Midas SPAC Merger Sub Inc., a Delaware corporation and previously a direct wholly-owned subsidiary of the Company prior to the Business Combination.

“SPAC Warrant Agreement” means the warrant agreement, dated as of September 28, 2021, by and between Red Rock and Continental, as amended on April 14, 2025.

“SPAC Sponsor” means Hennessy Capital Partners VI LLC, a Delaware limited liability company.

“Trading Day” means a day on which trading in the Ordinary Shares generally occurs on the principal U.S. national or regional securities exchange on which the Ordinary Shares are then listed or, if the Ordinary Shares are not then listed on a U.S. national or regional securities exchange, on the principal other market which the Ordinary Shares are then traded.

“Trading Volume” means, for any Trading Day, the daily trading volume for the Ordinary Shares, as reported by Bloomberg on such Trading Day.

“Warrant” means a warrant (i.e., a stock acquisition right) to purchase one Ordinary Share pursuant to the terms of the Warrant Agreement.

“Warrant Agreement” means the SPAC Warrant Agreement as modified by the Warrant Assumption Agreement.

“Warrant Assumption Agreement” means the Warrant Assumption Agreement, dated June 5, 2025, by and among the Company, Red Rock, and Continental.

“ZiG” means Zimbabwe Gold, the official currency of Zimbabwe.

xii

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus, including, without limitation, statements under the headings “Business” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” includes forward-looking statements within the meaning of Section 27A of the Securities Act and Section 21E of the Exchange Act. These forward-looking statements can generally be identified by the use of forward-looking terminology, including the terms “anticipates,” “believes,” “continues,” “could,” “estimates,” “forecasts,” “intends,” “expects,” “may,” “plans,” “predicts,” “projects,” “proposes,” “seeks,” “should,” “targets” or “will” or, in each case, their negative or other variations or comparable terminology. These forward-looking statements include all matters that are not historical facts.

The forward-looking statements in this prospectus are based on information available as of the date of this prospectus and are inherently subject to uncertainties and changes in circumstance and their potential effects and speak only as of the date of such statement. There can be no assurance that future developments will be those that have been anticipated. These forward-looking statements are not guarantees of future performance, conditions or results, and involve a number of known and unknown risks, uncertainties, assumptions and other important factors, many of which are outside the control of the Company, that could cause actual results or outcomes to differ materially from those discussed in the forward-looking statements. These risks and uncertainties include, but are not limited to, those factors described in the section entitled “Risk Factors” and the following important factors:

• market risks, including the price of gold;

• the outcome of any legal proceedings that may be instituted against the Company or any of its subsidiaries related to the Business Combination;

• the outcome of any legal proceedings relating to Greenstone’s purchase of Bulawayo Mining Company Limited, which owns all of the Company’s mines, from Metallon Corporation Limited;

• failure to realize the anticipated benefits of the Business Combination;

• the inability to maintain the listing of the Company’s securities on Nasdaq;

• the inability to remediate the identified material weaknesses in the Company’s internal control over financial reporting, which, if not corrected, could adversely affect the reliability of the Company’s financial reporting;

• the risk that the price of the Company’s securities may be volatile due to a variety of factors, including changes in the highly competitive industries in which the Company plans to operate, variations in performance across competitors, changes in laws, regulations, technologies, natural disasters or health epidemics/pandemics, national security tensions, macro-economic and social environments affecting its business, and changes in the combined capital structure;

• the inability to implement business plans, forecasts, and other expectations, identify and realize additional opportunities, and manage the Company’s growth and expanding operations;

• the risk that the Company may not be able to successfully develop its assets, including expanding the How Mine, restarting and expanding its other mines in Zimbabwe, or acquire and develop mining interests in the DRC;

• the risk that the Company will be unable to raise additional capital to execute its business plan, which may not be available on acceptable terms or at all;

• political and social risks of operating in Zimbabwe and the DRC; and

• the operational hazards and risks that the Company faces.

xiii

The risks outlined above and others described under the section entitled “Risk Factors” are not exhaustive. In addition, as a result of a number of known and unknown risks and uncertainties, including those listed above, the Company’s actual results or performance may be materially different from those expressed or implied by certain forward-looking statements. Should one or more of these risks or uncertainties materialize or should any of the assumptions made by the management team of the Company prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements.

Forward-looking statements reflect current beliefs and are based on information currently available as of the date a forward-looking statement is made. Accordingly, forward-looking statements set forth herein speak only as of the date of this Report.

The Company does not undertake any obligation to revise forward-looking statements to reflect future events, changes in circumstances, or changes in beliefs. In the event that any forward-looking statement is updated, no inference should be made that the Company will make additional updates with respect to that statement, related matters, or any other forward-looking statements.

xiv

PROSPECTUS SUMMARY

This summary highlights selected information contained elsewhere in this prospectus and does not contain all of the information you should consider when making your investment decision. Before investing in our securities, you should carefully read this entire prospectus, including our financial statements and the related notes included in this prospectus and the information set forth under the headings “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” See also the section entitled “Where You Can Find More Information.” The definition of some of the terms used in this prospectus are set forth under the section “Frequently Used Terms.” Unless the context otherwise requires, we use the terms “Namib Minerals,” “Company,” “we,” “us” and “our” in this prospectus to refer to Namib Minerals and its consolidated subsidiaries.”

Overview

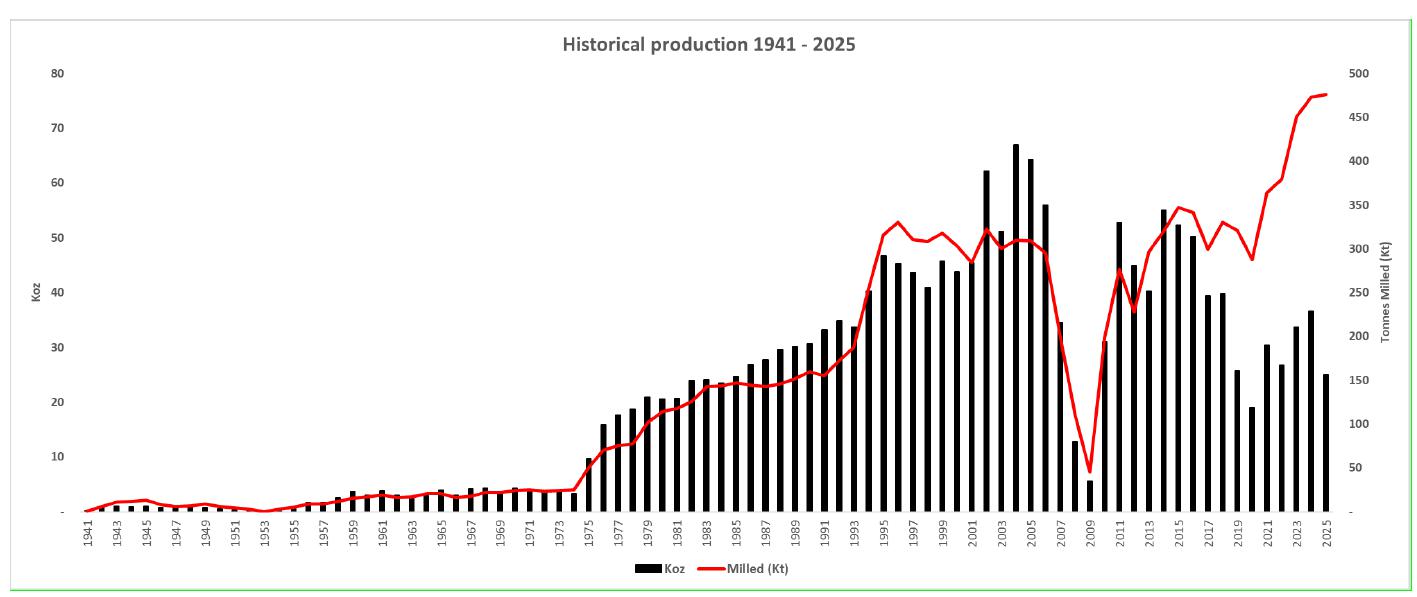

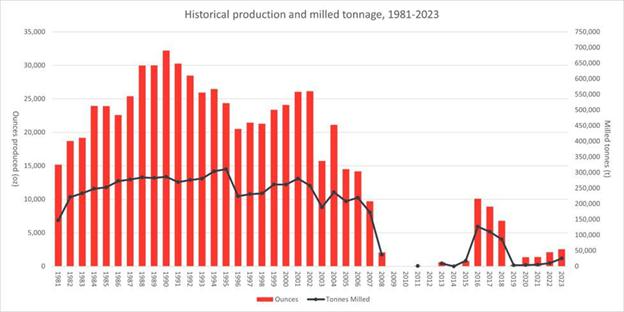

We are an established gold producer with an attractive portfolio of three gold mines in Zimbabwe, Africa. Our extensive track record of owning and operating gold mines spans over two decades, and our strategic footprint consists of one producing gold mine and two historically producing gold mines that we are currently positioning to restart operations. Our How Mine is an established underground gold mine with a strong track record of operations having produced an aggregate of approximately 1.84Moz of gold from 1941 through December 31, 2025. Our other principal assets, the Mazowe Mine and the Redwing Mine, are historically producing gold mines with significant mineral resources. These assets provide us with an identified pathway to operate as a multi-asset gold producer in Africa, as preparatory work is currently underway to restart operations at both mines. On a consolidated basis, combining our estimate as of December 31, 2025 for the How Mine and our estimates as of December 31, 2023 for the Mazowe Mine and the Redwing Mine, our underground measured and indicated gold resources (exclusive of reserves) totaled 2.5Moz at a grade of 2.26g/t Au and our underground inferred gold resources totaled 4.4Moz. We are also evaluating opportunities to acquire mining interests in, and expand our operations to, the Democratic Republic of Congo (“DRC”) to unlock critical battery metals in the region. For additional information regarding our business, see “Business.”

Corporate Information

The legal name of the Company is “Namib Minerals.” The Company was incorporated under the laws of the Cayman Islands on May 27, 2024 as an exempted company limited by shares with registration number 410406, having its registered office and mailing address for its principal executive office at Appleby Global Services (Cayman) Limited, Suite 210, 2nd Floor, Windward III, Regatta Office Park, PO Box 500, Grand Cayman, Cayman Islands, KY1-1106, and its telephone number is (345) 769-4909. Our principal website is https://www.namibminerals.com/. The information contained on, or that can be accessed through, our website is not incorporated by reference into, and is not a part of, this prospectus or the registration statement of which it forms a part.

1

The following depicts our organizational structure.

Emerging Growth Company

We qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”). For so long as we remain an emerging growth company, we are permitted, and currently intend, to rely on the following provisions of the JOBS Act that contain exceptions from disclosure and other requirements that otherwise are applicable to public companies and file periodic reports with the SEC. These provisions include, but are not limited to:

• the option to present only two years of audited financial statements and selected financial data and only two years of related “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in our periodic reports and registration statements, including this prospectus, subject to certain exceptions;

• not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act; and

• not being required to comply with any requirement that may be adopted by the PCAOB regarding mandatory audit firm rotation or a supplement to the auditor’s report providing additional information about the audit and the financial statements.

We will cease to be an “emerging growth company” upon the earliest to occur of: (i) the last day of the fiscal year in which we have more than $1.235 billion in annual revenue; (ii) the date we qualify as a large accelerated filer, with at least $700.0 million of equity securities held by non-affiliates; (iii) the date on which we have, in any three-year period, issued more than $1.0 billion in non-convertible debt securities; and (iv) December 31, 2030 (the last day of the fiscal year following the fifth anniversary of the Closing).

We have elected to take advantage of certain of the reduced disclosure obligations in this prospectus and may elect to take advantage of other reduced reporting requirements in our future filings with the SEC. As a result, the information that we provide to our stockholders may be different than what you might receive from other public reporting companies in which you hold equity interests.

2

Foreign Private Issuer

We report under the Exchange Act as a non-U.S. company with foreign private issuer status. Under Rule 405 of the Securities Act, the determination of foreign private issuer status is made annually on the last business day of an issuer’s most recently completed second fiscal quarter and, accordingly, the next determination will be made with respect to us on June 30, 2026. For so long as we qualify as a foreign private issuer, we will be exempt from certain provisions of the Exchange Act that are applicable to U.S. domestic public companies, including:

• the rules under the Exchange Act requiring the filing of quarterly reports on Form 10-Q, current reports on Form 8-K with the SEC or annual reports on Form 10-K;

• the sections of the Exchange Act regulating the solicitation of proxies, consents, or authorizations in respect of a security registered under the Exchange Act; and

• the selective disclosure rules by issuers of material nonpublic information under Regulation Fair Disclosure, or Regulation FD, which regulates selective disclosure of material non-public information by issuers

We may take advantage of these exemptions until such time as we are no longer a foreign private issuer. We would cease to be a foreign private issuer at such time as more than 50% of our outstanding voting securities are held by U.S. residents and any of the following three circumstances applies: (i) the majority of our executive officers or directors are U.S. citizens or residents, (ii) more than 50% of our assets are located in the United States or (iii) our business is administered principally in the United States. See “Management — Foreign Private Issuer Exemption.”

In addition, as a foreign private issuer, the Company is permitted to follow certain Cayman Islands corporate governance practices in lieu of certain corporate governance rules of Nasdaq. However, the Company currently plans to follow the corporate governance requirements of Nasdaq.

Controlled Company

The SelliBen Trust owns approximately 63% of the issued and outstanding Ordinary Shares. As a result, the Company qualifies as a “controlled company” as defined under the corporate governance rules of Nasdaq, because the SelliBen Trust beneficially owns greater than 50% of the total voting power of all issued and outstanding Ordinary Shares. Under the applicable Nasdaq rules, a controlled company may elect not to comply with certain corporate governance requirements, including the requirement that a majority of its directors be independent and the requirement that the compensation committee and nominating and corporate governance committee consist entirely of independent directors. The Company currently does not intend to rely on these exemptions. However, if the Company decides to rely on exemptions applicable to controlled companies under the Nasdaq rules in the future, its shareholders will not have the same protections afforded to shareholders of companies that are subject to all of the Nasdaq corporate governance requirements. See “Management — Controlled Company.”

Risk Factor Summary

You should consider all of the information contained in this prospectus before investing in our securities which involves substantial risk. Our business is subject to numerous risks and uncertainties, including those highlighted in the section entitled “Risk Factors” beginning on page 7 of this prospectus, that represent challenges that we face in connection with the successful implementation of our strategy and the growth of our business. The occurrence of one or more of the events or circumstances described in the section entitled “Risk Factors,” alone or in combination with other events or circumstances, may have a material adverse effect on our business, cash flows, financial condition and results of operations. Important factors and risks that could cause actual results to differ materially from those in the forward-looking statements include, among others, the following:

Risks Related to Our Business, Operations and Industry

• We are subject to risks related to the development of existing and new mining projects that may adversely affect our results of operations and profitability.

• We require significant additional capital to fund our business, and no assurance can be given that such capital will be available at all or available on terms acceptable to us.

3

• Our Mineral Resource and Mineral Reserve estimates may be materially different from mineral quantities we may ultimately recover, our life-of-mine estimates may prove inaccurate, and changes in operating and capital costs may render mineral resources uneconomic to mine.

• Mining is inherently hazardous and the related risks of events that cause disruptions to our mining operations may adversely impact the environment or the health, safety, or security of our workers or the local community, production, cash flows, and overall profitability.

• Our assets and operations are subject to political, economic, and other uncertainties as a result of being located in Zimbabwe.

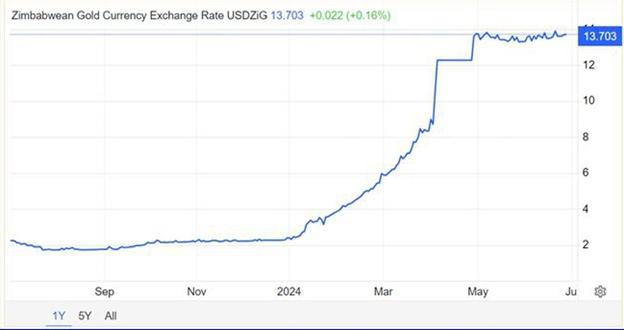

• Fluctuating foreign currency and exchange rates as well as Zimbabwean exchange controls may negatively impact our business, results of operations, and financial position.

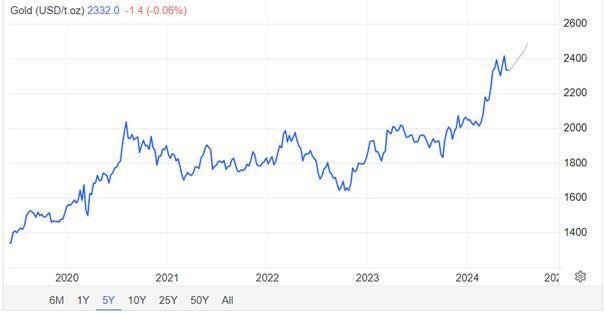

• The price of gold is subject to volatility and may have a significant effect on our future activities and profitability.

• Our operations are vulnerable to infrastructure constraints, including power and water supply.

• We derive all of our revenues from the sale of gold to one company which is controlled by the Zimbabwean authorities. There is no assurance that such counterparty may not default in such obligation causing us to incur a financial loss.

• Our rights to mine in Zimbabwe are derived from each of the How Mine Lease, the Mazowe Mine Lease, and the Redwing Mine Lease, the loss of which would have a material adverse effect on our financial condition and results of operations.

• Since operations at our Mazowe Mine and Redwing Mine were halted in 2018 and 2019, respectively, we have been subject to litigation regarding disputed debts and corporate rescue proceedings pursuant to Zimbabwean insolvency laws.

• Greenstone’s purchase of the Mazowe Mine, the Redwing Mine, and the How Mine from Metallon may be subject to potential claims that may have a material adverse effect on the Company’s assets and operations.

Risks Related to Cybersecurity

• Cybersecurity breaches and other disruptions or failures in our information technology systems could compromise our information, result in the unauthorized disclosure of confidential supplier, employee, and Company information, damage our reputation, and expose us to liability.

Risks Related to Laws and Regulations

• Our operations are subject to various government approvals, permits, licenses, and legal regulation for which no assurance can be provided that such approvals, permits, or licenses will be obtained or if obtained will not be revoked or suspended.

• Failure to comply with the U.S. Foreign Corrupt Practices Act and similar laws in Zimbabwe and elsewhere associated with our activities could subject us to penalties and other adverse consequences.

Risks Related to the Ownership of Our Securities and General Matters

• There can be no assurance that we will be able to maintain compliance with the continued listing standards of Nasdaq over time.

• Future sales or resales of a substantial number of our Ordinary Shares, or the perception in the market that the holders of a large number of Ordinary Shares intend to sell shares, could reduce the market price of our Ordinary Shares.

• The Company incurs additional costs as a result of operating as a public company, and its management devotes substantial time to ongoing compliance requirements.

4

• The SelliBen Trust owns the majority of our issued and outstanding Ordinary Shares, which provides it the right to appoint a majority of the members of the Company Board. Accordingly, its interests may conflict with those of our other shareholders, which may have the effect of delaying or preventing a change in control.

• We do not intend to pay cash dividends for the foreseeable future and, as a result, your ability to achieve a return on your investment will depend on appreciation in the price of our Ordinary Shares.

• We are a holding company. Our only significant asset is our ownership of 100% of the securities of Greenstone, and we will accordingly be dependent on distributions from Greenstone and its subsidiaries to meet our financial obligations and to pay dividends, if any.

• We have identified material weaknesses in our internal control over financial reporting. If we are unable to remediate these material weaknesses, or if we identify additional material weaknesses in the future, or we otherwise fail to implement and maintain an effective system of internal controls, we may be unable to accurately or timely report our results of operations or prevent fraud, and investor confidence and the market price of our Ordinary Shares may be materially and adversely affected.

• As an “emerging growth company” within the meaning of the Securities Act and the Exchange Act, we may take advantage of certain exemptions from disclosure requirements available to emerging growth companies, which may make our securities less attractive to investors and more difficult to compare our performance to the performance of other public companies.

Risks Related to an Investment in a Cayman Company and the Company’s Status as a Foreign Private Issuer

• As a foreign private issuer, we are exempt from a number of U.S. securities laws and rules promulgated thereunder and will be permitted to publicly disclose less information than U.S. public companies must. This may limit the information available to holders of our Ordinary Shares.

• Your ability to protect your rights through U.S. courts may be limited as we are incorporated under the law of the Cayman Islands. We conduct substantially all of our operations, and half of our directors and executive officers reside, outside of the United States.

5

THE OFFERING

Resale of Ordinary Shares

|

Ordinary Shares offered by the Selling Shareholder |

|

|

|

Terms of the offering |

The Selling Shareholder will determine when and how it will dispose of the Ordinary Shares registered for resale under this prospectus. See “Plan of Distribution.” |

|

|

Use of proceeds |

We will not receive any of the proceeds from the sale of Ordinary Shares by the Selling Shareholder. |

|

|

Nasdaq ticker symbol |

Our Ordinary Shares are listed for trading on the Nasdaq Global Market under the symbol “NAMM.” |

|

|

Risk factors |

Any investment in the Ordinary Shares offered hereby is speculative and involves a high degree of risk. You should carefully consider the information set forth under “Risk Factors” and elsewhere in this prospectus. |

6

RISK FACTORS

Investing in our securities involves risks. In considering purchasing our securities, you should carefully consider the following information about these risks, as well as the other information included in this prospectus. The risks and uncertainties described below are those significant risk factors, currently known and specific to us, that we believe are relevant to an investment in our securities. Additional risks and uncertainties not presently known to us or that we currently deem immaterial may also harm us and adversely affect our securities The occurrence of one or more of the events or circumstances described in these risk factors, alone or in combination with other events or circumstances, may have a material adverse effect on our business, reputation, revenue, financial condition, results of operations, and future prospects, in which event the market price of our securities could decline, and you could lose part or all of your investment.

Risks Related to Our Business, Operations and Industry

We are subject to risks related to the development of existing and new mining projects that may adversely affect our results of operations and profitability.

Development of our existing and new mining projects may be subject to unexpected problems, costs, and delays that could impact our ability to develop or operate the relevant project as planned. For example, constraints on the supply of mining and processing equipment, increases in capital and operating costs, or reduced availability of utilities could result in delays in completing projects.

We are currently engaged in further development activities at the How Mine, the Mazowe Mine, and the Redwing Mine. The Mazowe Mine and the Redwing Mine are currently under care and maintenance and work is currently underway to restart operations there. Estimates and targets for future production at these sites are based on technical expertise, historical production, mining plans, and an understanding of the orebody of each and are subject to change. Production estimates and production targets are subject to risks associated with our mining operations and, as a result, no assurance can be given that future production estimates or targets will be achieved. Actual production may vary from estimated or targeted production for reasons which we may not be able to control.

Ultimately, we may prove unable to successfully operate existing mine sites, restart our Mazowe Mine and Redwing Mine which have paused operations since 2018 and 2019, respectively, or to develop potential exploration sites due to, for example, unanticipated variations in mined tonnages and geological conditions, accident, plant and equipment breakdown, expiration of useful life, obsolescence, replacement, changes in metal prices, changes in the cost and supply of inputs, social and community opposition, vandalism, theft, destruction, encroachment, title challenges, litigation, governmental regulatory or administrative proceedings, changes in applicable regulations or other requirements, the classification of land covered by mining titles as an environmentally-protected area, ore body grades, the inability of any such project to meet our investment hurdle rate, and delays or the inability of obtaining or renewing permits. For example, while our Mazowe Mine and Redwing Mine have been under care and maintenance programs, many of the related operational permits have expired and will need to be renewed or reissued before commercial operations may resume. Failure to comply with these requirements could result in enforcement proceedings, claims, suspension of operations, community protest and/or additional capital or operating expenditures that could adversely impact our financial condition or reputation. The remote location of mining properties, delays in obtaining or failure to obtain necessary environmental and other governmental permits and approvals, the impact of public health crises, epidemics or pandemics (for example, the Mpox epidemic, particularly in Africa, and the COVID-19 pandemic) as well as third-party legal challenges to individual mining projects and broader social or political opposition to mining may increase the cost, timing and complexity of mine development and construction.

Accordingly, our future development activities may not result in the expansion or replacement of current production, or one or more production sites or facilities may not be developed as planned or may be less profitable than anticipated or even be loss-making. A failure in our ability to develop and operate mining projects in accordance with, or in excess of, expectations could negatively impact its results of operations, as well as its financial condition and prospects.

7

We require significant additional capital to fund our business, and no assurance can be given that such capital will be available at all or available on terms acceptable to us.

We require a substantial amount of capital to progress and develop our metals mining business. Mining requires a substantial amount of capital in order to identify and delineate mineral resources through geological mapping and drilling, identify geological features that may prevent or restrict the extraction of ore, construct extraction and processing facilities, expand production capacity, replenish reserves, purchase, maintain and improve assets, equipment, buildings, plants and other infrastructure, comply with legal or regulatory requirements or industry standards, and meet unexpected liabilities. Large amounts of capital are required to implement projects, and long-term production and processing require both significant capital expenditures and ongoing maintenance and working capital expenditures.

A substantial amount of capital will be required to restart the Mazowe Mine and the Redwing Mine, which have been in care and maintenance and not operational since 2018 and 2019, respectively, and expand such historical operations, including plant processing capacity. Such capital expenditures are anticipated to include expenditures for feasibility studies, upgrading infrastructure, pumping out water that has flooded a portion of the mines, environmental assessments, procuring and restoring equipment, and recommencing commercial operations. These capital expenditures do not include any taxes or other required payments outstanding from the Mazowe Mine and the Redwing Mine being placed in care and maintenance, such as social program funding obligations. We also expect to materially increase our capital expenditures to support the growth in our business and operations at our How Mine. We may also require additional capital to fund potential acquisitions in the DRC or elsewhere going forward.

Our business is based on, among other things, expectations as to future capital expenditures, and if we are unable to fund those capital expenditures, as a result of our operations being unable to generate sufficient cash flow or as a result of difficulties in raising debt or equity funding on acceptable terms or at all, we will not be able to recommence operations of the Redwing Mine and the Mazowe Mine at the planned capacity, or at all, or be able to develop future capital projects. In addition, we may be unable to develop new capital projects to continue production at cost-effective levels. Furthermore, any such reduction in capital expenditures may cause us to forgo some of the benefits of any future increases in commodity prices, as it is generally costly or impossible to resume production immediately or complete a deferred expansionary capital expenditure project.

As of December 31, 2025, we had cash and cash equivalents of $1.9 million and negative working capital of $(37.4) million.

It is possible that we will borrow money to finance future capital expenditures or for other uses. Our capital expenditures financed by borrowing may increase our leverage and make it more difficult for us to satisfy our obligations, limit our ability to obtain additional financing to operate our business, or require us to dedicate a substantial portion of our cash flow to make payments on our debt. This may reduce our ability to use our cash flow to fund working capital, capital expenditures, and other general corporate requirements.

Any future debt we incur and other agreements we enter into may contain, among other provisions, covenants that restrict our ability to finance future operations or capital needs or to engage in other business activities. Given the long-term nature of such agreements, these covenants and restrictions may present a material constraint on our operational and strategic flexibility and may preclude us from entering into strategic transactions that would be beneficial to us. A breach of any of these covenants could result in an event of default under the relevant agreement, and any such event of default or resulting acceleration under such agreements could result in an event of default under other agreements.

Our Mineral Resource and Mineral Reserve estimates may be materially different from mineral quantities we may ultimately recover, our life-of-mine estimates may prove inaccurate, and changes in operating and capital costs may render mineral resources uneconomic to mine.

We have reported our mineral resources in accordance with the requirements of the Modernization of Property Disclosures for Mining Registrants set forth in Regulation S-K 1300. There are numerous uncertainties inherent in estimating quantities of mineral resources and in projecting potential future mineral reserves and rates of mineral production, including many factors beyond our control. The accuracy of any mineral resource and mineral reserves estimate is a function of a number of factors, including the quality of the methodologies employed, the quality and quantity of available data and geological interpretation and judgment, and is also dependent on economic conditions, such as commodity prices and exchange rates, and market prices being generally in line with estimates.

8

Furthermore, estimates of different geologists and mining engineers may vary, and results of our mining and production subsequent to the date of an estimate may lead to revision of estimates due to, for example, fluctuations in the market price of ores and metals, reduced metal recovery or increased production costs due to inflation or other factors which may render mineral resources containing lower grades of mineralization uneconomic to exploit and may ultimately result in a restatement of mineral resources and may adversely impact future cash flows. Mineral Resource and Mineral Reserve estimates are based on limited sampling and, consequently, are uncertain as the samples may not be representative of the entire body of mineralization. As a better understanding of a body of mineralization is obtained, the estimates may change significantly. The mineral reserves we ultimately exploit may not conform to geological, metallurgical, or other expectations and the volume and grade of ore recovered may be below the estimated levels. Mineral resources data is not indicative of future production.

Developing new properties requires substantial capital expenditures to identify and delineate mineral resources through geological and geotechnical surveying and drilling, to identify geological features that may prevent or restrict the extraction of ore, to determine the metallurgical processes to extract the metals from the ore, and to construct mining and processing facilities. Accordingly, it may not always be possible or economical to conduct such exercises at regular intervals or at all in the future.